Futures Market: On Friday evening, LME copper opened at $9,375.5/mt. It initially dipped to $9,350/mt, fluctuated considerably during the session, hitting a high of $9,401.5/mt, and eventually closed at $9,360/mt after continued fluctuations, down 1%. Trading volume reached 13,000 lots, and open interest stood at 286,000 lots. On the same evening, the most-traded SHFE copper 2506 contract opened at 77,510 yuan/mt. It fluctuated rangebound in the early session, with the price center moving lower, hitting a low of 77,250 yuan/mt. The price center rebounded towards the end of the session, reaching a high of 77,550 yuan/mt, and eventually closed at 77,470 yuan/mt, down 0.22%. Trading volume reached 45,000 lots, and open interest stood at 162,000 lots. On the macro front, US stocks generally had a mediocre performance on Friday, with market participants continuing to await more information on the tariff war.

【SMM Copper Morning Meeting Summary】News: (1) Chile's state-owned copper company Codelco stated that its total production in Q1 this year was 296,000 mt, up 0.3% YoY. Despite facing various challenges in Q1, including a regional rainy season and a nationwide power outage in February that reduced refined copper production by 10,000 mt, the company still achieved this growth, according to its statement.

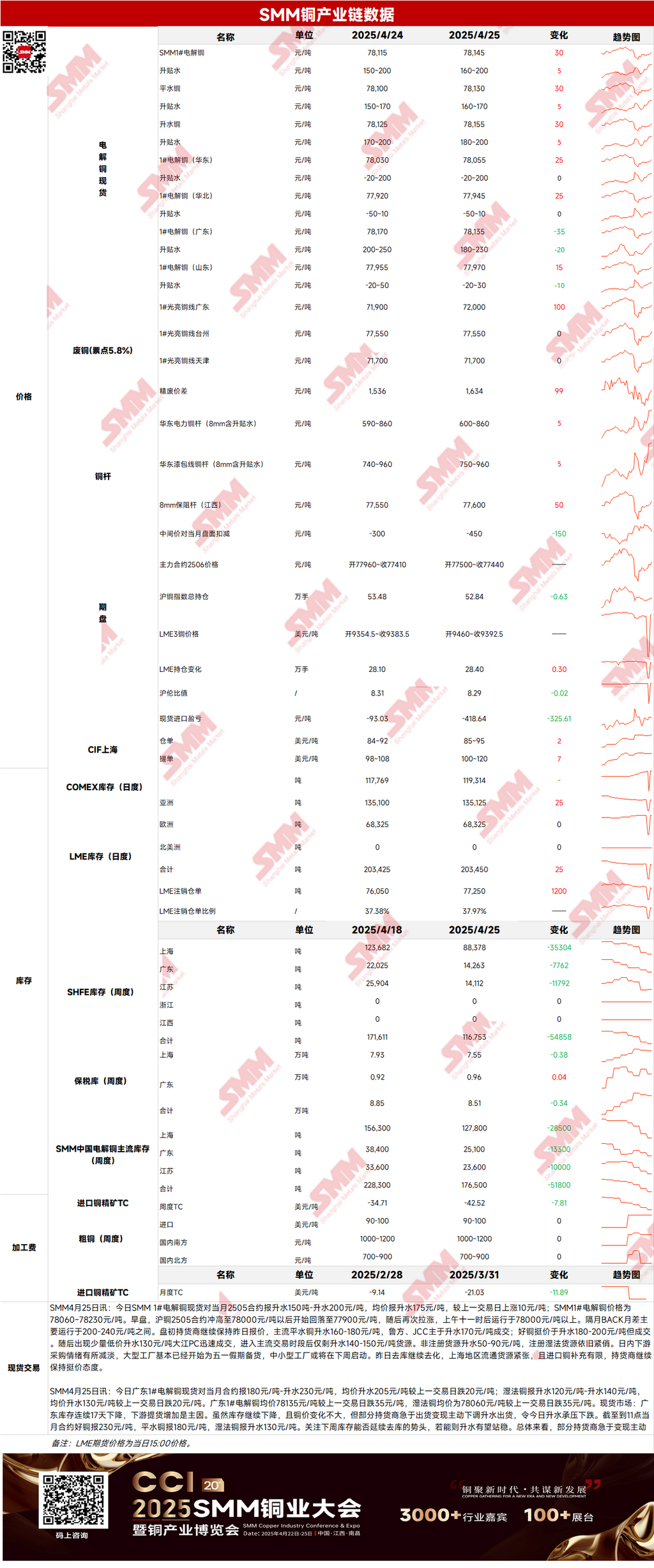

Spot: (1) Shanghai: On April 25, SMM #1 copper cathode spot prices against the front-month 2505 contract were reported at a premium of 150-200 yuan/mt, with an average premium of 175 yuan/mt, up 10 yuan/mt from the previous trading day. The SMM #1 copper cathode price was 78,060-78,230 yuan/mt. In the morning session, after the SHFE copper 2505 contract surged to 78,000 yuan/mt, it pulled back to 77,900 yuan/mt before rallying again, trading above 78,000 yuan/mt after 11 a.m. The backwardation between the front-month and next-month contracts mainly ranged between 200-240 yuan/mt.

(2) Guangdong: On April 25, Guangdong's #1 copper cathode spot prices against the front-month contract were reported at a premium of 180-230 yuan/mt, with an average premium of 205 yuan/mt, down 20 yuan/mt from the previous trading day. SX-EW copper was reported at a premium of 120-140 yuan/mt, with an average premium of 130 yuan/mt, down 20 yuan/mt from the previous trading day. The average price of Guangdong's #1 copper cathode was 78,135 yuan/mt, down 35 yuan/mt from the previous trading day, and the average price of SX-EW copper was 78,060 yuan/mt, down 35 yuan/mt from the previous trading day. Overall, some suppliers were eager to liquidate their positions and actively lowered prices, leading to a decline in spot premiums.

(3) Imported Copper: On April 25, warrant prices were $85-95/mt, with a QP of May, and the average price increased by $2/mt from the previous trading day. B/L prices were $100-120/mt, with a QP of May, and the average price increased by $7/mt from the previous trading day. EQ copper (CIF B/L) prices were $60-70/mt, with a QP of May, and the average price remained unchanged from the previous trading day. Quotations referenced cargoes arriving in late April and early May. Since the day before yesterday, it was heard that overseas traders had resumed seeking CME-registered cargoes arriving in late April and early May, with suppliers showing a clear sentiment to stand firm on quotes. Meanwhile, the transaction center for EQ cargoes moved higher, with transactions significantly more active than in previous days.

(4) Secondary Copper: On April 25, the price of secondary copper raw materials increased by 100 yuan/mt MoM. The price of bare bright copper in Guangdong was 71,900-72,100 yuan/mt, up 100 yuan/mt MoM from the previous trading day. The price difference between copper cathode and copper scrap was 1,634 yuan/mt, up 98 yuan/mt MoM. The price difference between copper cathode rod and secondary copper rod was 1,180 yuan/mt. According to an SMM survey, European import supplies remained tight. A Ningbo-based import trader stated that European bare bright copper quotation coefficients were still at 99%-99.5% this week. Although the import window for secondary copper raw materials is currently open, domestic scrap utilisation enterprises still cannot accept the high prices of secondary copper raw materials. Therefore, No.1 copper and No.2 copper are currently more favored by domestic scrap utilisation enterprises. Unless copper prices continue to rise, further widening the price difference between copper cathode and copper scrap, domestic scrap utilisation enterprises will only consider purchasing imported bare bright copper.

(5) Inventory: On April 25, LME copper cathode inventory increased by 25 mt to 203,450 mt. On the same day, SHFE warrant inventory decreased by 1,376 mt to 41,588 mt.

After Trump stated that he would consider it a "complete victory" if import tariffs reached 50% within a year, market sentiment remained somewhat uneasy. However, the overall market sentiment remained cautious due to the deteriorating economic outlook and tariffs that were hurting corporate profits. The US dollar recorded its first weekly gain since mid-March, putting pressure on copper prices. On the fundamental side, from the supply side, minor losses in SHFE copper imports have led to tight arrivals, coupled with limited replenishment of circulating supplies in the Shanghai area after destocking, causing suppliers to maintain a sentiment to stand firm on quotes. From the demand side, large factories have largely completed their stockpiling for the May Day holiday, while small and medium-sized enterprises began stockpiling this week. Additionally, with copper prices at high levels, downstream buyers are hesitant due to factors such as tariffs, and cautious purchasing has suppressed transactions. In terms of prices, the US Fed is still finding it difficult to cut interest rates, and its outlook remains vague, raising market concerns that the Fed may only take action after a US economic recession actually occurs. Copper prices are already under pressure from the current situation, and with a series of economic data to be released this week, copper prices may experience significant volatility.

【The information provided is for reference only. This article does not constitute direct investment research and decision-making advice. Clients should make cautious decisions and not rely on this as a substitute for independent judgment. Any decisions made by clients are unrelated to SMM.】